[For the latest information on CHIP, see CCF’s CHIP page.]

ABOUT CHIP

Introduction

In 1997, the Children’s Health Insurance Program (CHIP) was created with strong bipartisan support. CHIP gives states financial support to expand publicly funded coverage to uninsured children who are not eligible for Medicaid. As a block grant, CHIP provides states with a set amount of funding that must be matched with state dollars.

The Children’s Health Insurance Program Reauthorization Act (CHIPRA) reauthorized CHIP in April 2009 and the 2010 Affordable Care Act (ACA) contained provisions to strengthen the program. The ACA extended CHIP funding until September 30, 2015 and requires states to maintain eligibility standards through September 30, 2019. The Medicare Access and CHIP Reauthorization Act (MACRA) of 2015 extended CHIP funding with no programmatic changes through September 30, 2017. Legislative action will be required to extend federal funding past September 2017.

This primer provides a general overview of the program structure and rules for CHIP. Additional resources on CHIP are available here. Also see our Facts & Statistics for eligibility and program rules by state.

Structure

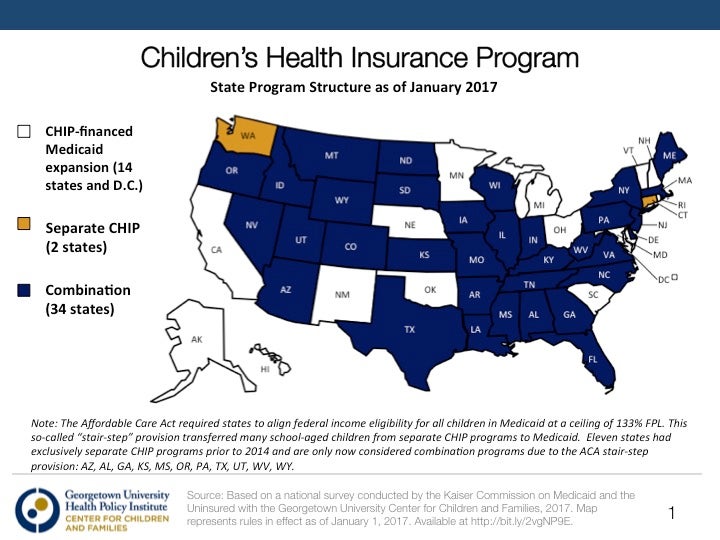

CHIP builds on Medicaid’s success providing health coverage to children since 1965. States can use their federal CHIP funds to finance coverage for children whose family incomes are too high to qualify for Medicaid under the rules the state had in place as of June 1997. States may opt to use CHIP funds to expand Medicaid for children beyond the June 1997 levels, cover children through a separate CHIP program, or combine the two approaches. As of January 1 2017, 15 states (including the District of Columbia) opted to use CHIP funds to expand their Medicaid programs. In the remaining 36 states, map here, CHIP funds are used to run a combination or separate health insurance program.

During FY 2016, 8.9 million children were ever enrolled in coverage funded by CHIP while 37.1 million children were ever enrolled in Medicaid-financed coverage. In 2015, more than half (56%) of children with CHIP are actually enrolled in expanded Medicaid coverage financed by CHIP. Also in 2015, CHIP spending reached over $13.5 billion, compared to a total of $524 billion in Medicaid.

Financing

Federal and state governments jointly finance CHIP, although the federal government assumes a larger share of the financing with an enhanced federal matching rate ranging from 65 to 82 percent, an average of 15 percentage points higher than Medicaid’s matching rate. The ACA (2010) established, and MACRA (2015) funded, a boost to the CHIP enhanced matching rate of an additional 23 percentage points up to a 100 percent maximum through 2017. Unlike Medicaid, CHIP funds are capped overall and for each state. This capped funding is distributed through state-specific allotments established by a statutory formula that accounts for the state’s actual use of CHIP funds and is adjusted for health care inflation and child population growth. States facing funding shortfalls can obtain additional funding through a child enrollment contingency fund and allotment increases are available for states with approved plans to expand eligibility or benefits.

CHIP funds generally must be used to provide coverage to uninsured, low‐income children who do not qualify for Medicaid. States also can use a limited amount of funds for administrative costs and other non‐coverage activities, such as outreach.

Eligibility

Federal CHIP eligibility rules set the guidelines determining which children states can cover with federal CHIP funds. In Medicaid‐expansion states, children who cannot be covered with CHIP funds may, in certain situations, be covered with Medicaid funds. In order to qualify, children must meet certain eligibility criteria that are outlined below. (See state-specific information on eligibility levels here.)

Income

| Minimum Eligibility | |

| Children | States have broad flexibility to set their CHIP income eligibility levels. Most states cover children up to or above 200 percent of the federal poverty level (FPL); the median across states is 255 FPL. States expanding coverage up to 300 percent of the FPL receive an enhanced federal match rate. States opting to expand coverage to children above 300 percent on or after FY 2009 receive the regular Medicaid match for their coverage. |

| Pregnant Women | CHIPRA (2009) allowed a state to amend its CHIP plan to cover pregnant women with CHIP funds. States using their CHIP plan to cover pregnant women must cover up to at least 185 percent of FPL. The income eligibility level must also be equal to or greater than income limits in Medicaid. This coverage is eligible for the enhanced federal match. Currently, 20 states offer coverage to pregnant women funded by CHIP. |

| Parents and Other Adults | CHIP law does not allow coverage of parents and adults. Although a handful of states previously obtained waivers from the federal government to cover uninsured adults and parents, these waivers expired and are no longer allowed in CHIP. States may be able to receive funding outside of CHIP to continue coverage for those already enrolled. |

| Age

|

States may cover children up to 19 years of age.

|

Insurance Status

Children must be uninsured to qualify for CHIP coverage. Some states impose waiting periods, which require children to be uninsured for a certain period of time before they can enroll, but this is not a federal requirement. As of January 2017, 15 states imposed waiting periods.

Citizenship/Immigration Status

CHIP covers citizens and certain legal immigrants. Under CHIPRA, states gained the option to cover lawfully residing immigrant children who have not been in the country for five years (with exceptions for refugees). As of July 2017, 32 states and D.C. have taken this option for children. Federal funds may not be used to cover undocumented children (except for emergency or pregnancy‐related services). Some states use state funding to cover children regardless of immigration status.

Application and Enrollment

Coordination

States with separate CHIP programs must coordinate their enrollment procedures with Medicaid to prevent children from “falling through the cracks” and remaining uninsured, as well as to ensure enrollment in the appropriate program. These coordination rules require state CHIP programs to screen CHIP applicants for both Medicaid and CHIP eligibility to assure that Medicaid‐eligible children are enrolled into Medicaid, and not simply turned away from CHIP. This “screen and enroll” requirement also applies to Medicaid and the ACA marketplaces to assure they screen for CHIP eligibility, in accordance with the ACA’s “No Wrong Door” requirement.

Streamlining and Enrollment

States are provided with several policy options for streamlining enrollment. Express lane eligibility allows states to rely on eligibility determinations made by other public programs (e.g., State Nutrition Assistance Program, or SNAP, School Lunch, Temporary Assistance to Needy Families, or TANF) to determine whether a child is eligible for Medicaid or CHIP. This approach provides administrative efficiencies while simultaneously preventing families from having to provide the same information to multiple agencies. Presumptive eligibility (PE) allows qualified entities (e.g., physicians, hospitals, schools) to make a preliminary eligibility decision. PE allows eligible individuals to get immediate coverage of health services while the regular application process is completed. PE is open to pregnant women, children, and adults.

Verification and Documentation

As of 2014, states are expected to rely on trusted electronic data sources rather than paper documentation to verify eligibility. Only when information cannot be obtained through an electronic data source or is not ‘‘reasonably compatible’’ with information provided by the consumer can additional information, including paper documentation, be requested. States must verify income electronically; however, this can be done post-enrollment after the state determines eligibility based on the individual’s self-attestation. The only eligibility criterion that federal law requires families to document is immigration and citizenship status.

Renewal

Under the ACA, state agencies can review eligibility no more often than once every 12 months. Additionally, states can provide children with a full 12-months of coverage, regardless of fluctuations in income, through the continuous eligibility option. Beginning in 2014, states are expected to automatically renew enrollees by determining eligibility based on a review of existing data.

Benefits

If a state has elected to use its CHIP funds to expand Medicaid coverage for children, the Medicaid program rules on benefits and the scope of coverage will apply to the group of children covered under the expansion in the same manner that they apply to children already eligible under the Medicaid program. However, if a state elects to use its CHIP funds to cover children under a separate state program, states have other options for meeting minimum federal benefit standards.

States can choose health benefits coverage equivalent to those offered under:

- The standard Blue Cross/Blue Shield preferred provider option offered to federal employees;

- A health plan available to a state’s public employees; or

- The HMO within the state that has the highest commercial enrollment (excluding Medicaid enrollment).

A state can also choose one of these three plans to serve as a “benchmark” for an alternative package of benefits. Finally, federal officials have the authority to allow states to use alternative benefit packages if they determine that they are appropriate for low‐income children. CHIPRA made dental services a mandatory benefit for states with separate CHIP plans, and gave states the option to provide supplemental dental coverage to CHIP-eligible children with private coverage that does not provide dental.

States also have the option to use CHIP funds for “premium assistance,” which helps families with the cost of private insurance rather than covering children in traditional CHIP coverage.

Premiums and Cost-sharing

States may impose cost-sharing (i.e., deductibles, coinsurance, and co‐payments) for some children enrolled in CHIP, within federal guidelines.

In general, states cannot adopt cost-sharing or premium policies that impose costs that exceed five percent of family income or that favor higher‐income families over lower‐income families. They also are prohibited from imposing cost-sharing for well‐baby and well‐child care, including immunizations. Finally, states cannot count money raised through premiums or cost-sharing as state dollars for purposes of meeting the block grant’s matching requirements.

Research has shown that premiums in Medicaid and CHIP depress enrollment because of the financial burden they impose on families, potentially increasing the number of uninsured children.

{kind=link}