The cost of health care is a critical concern during the current pandemic. People who worry about out-of-pocket costs are more reluctant to seek care. For those with private health insurance, out-of-pocket costs may take the form of deductibles, copayments, or coinsurance. When receiving services from an out-of-network provider, patients may also face balance bills (amounts billed by the out-of-network provider when insurers do not pay their full charges). When an individual faces high costs for seeking COVID-19 related services, it is not only a concern for that person, but a public health threat to everyone.

People are more likely to use out-of-network facilities and providers during the pandemic. If some hospitals are at capacity, patients may be sent to other hospitals. Temporary testing sites and clinics have also been created to handle the crisis. Workforce shortages mean that hospitals are bringing in new physicians and other health care professionals to treat patients. There is a risk many of these new testing sites and health professionals will not be in consumers’ insurance networks.

Fortunately, many COVID-19 patients are not facing cost sharing. The federal Families First and CARES Acts mostly eliminated cost sharing for an evaluation visit where a coronavirus test is ordered and for the test itself. And many insurers are voluntarily eliminating cost sharing for most COVID-related diagnosis, testing, and treatment.

In addition, there is some protection from balance billing for COVID-19 related health care services. The Trump Administration has required providers to forgo balance billing if they accept the Provider Relief Funds (PRF) to assist providers who are losing revenues or incurring added expenses due to COVID-19. Yet questions remain about the breadth of the balance billing protections.

The Provider Relief Fund Comes With Strings Attached

The CARES Act made $100 billion in Provider Relief Funds (PRF) available to hospitals and other health care providers to reflect lost revenue due to the pandemic or added expenses incurred in treating COVID-19 patients. An additional $75 billion was authorized in the Paycheck Protection Program and Health Care Enhancement Act (PPPHCEA), also known as stimulus bill “3.5.” The Trump administration subsequently announced that a portion of PRF dollars will be available to reimburse providers who treat uninsured COVID-19 patients.

The terms and conditions for accepting PRF payments prohibit providers from balance billing COVID-19 patients, regardless of their source of coverage. A provider accepting these funds must certify “that it will not seek to collect from the patient out-of-pocket expenses in an amount greater than what the patient would have otherwise been required to pay” for in-network services. This ban on balance billing takes protections well beyond the provisions of the CARES Act, but there remains uncertainty about how thoroughly these terms and conditions will protect patients.

Scope of Balance Billing Protections Under the Provider Relief Fund

We do not know precisely which patients, with which diagnoses, and for what services, will qualify for protection from balance bills under this new program. Similarly, there is no clear way for patients to know which providers will receive the funds and thus which providers are barred from sending balance bills. It is also not clear how private insurers will compensate an out-of-network provider in this program, if they know the provider is barred from sending any bills directly to the patient.

Are All Patients and Services Protected from Balance Billing?

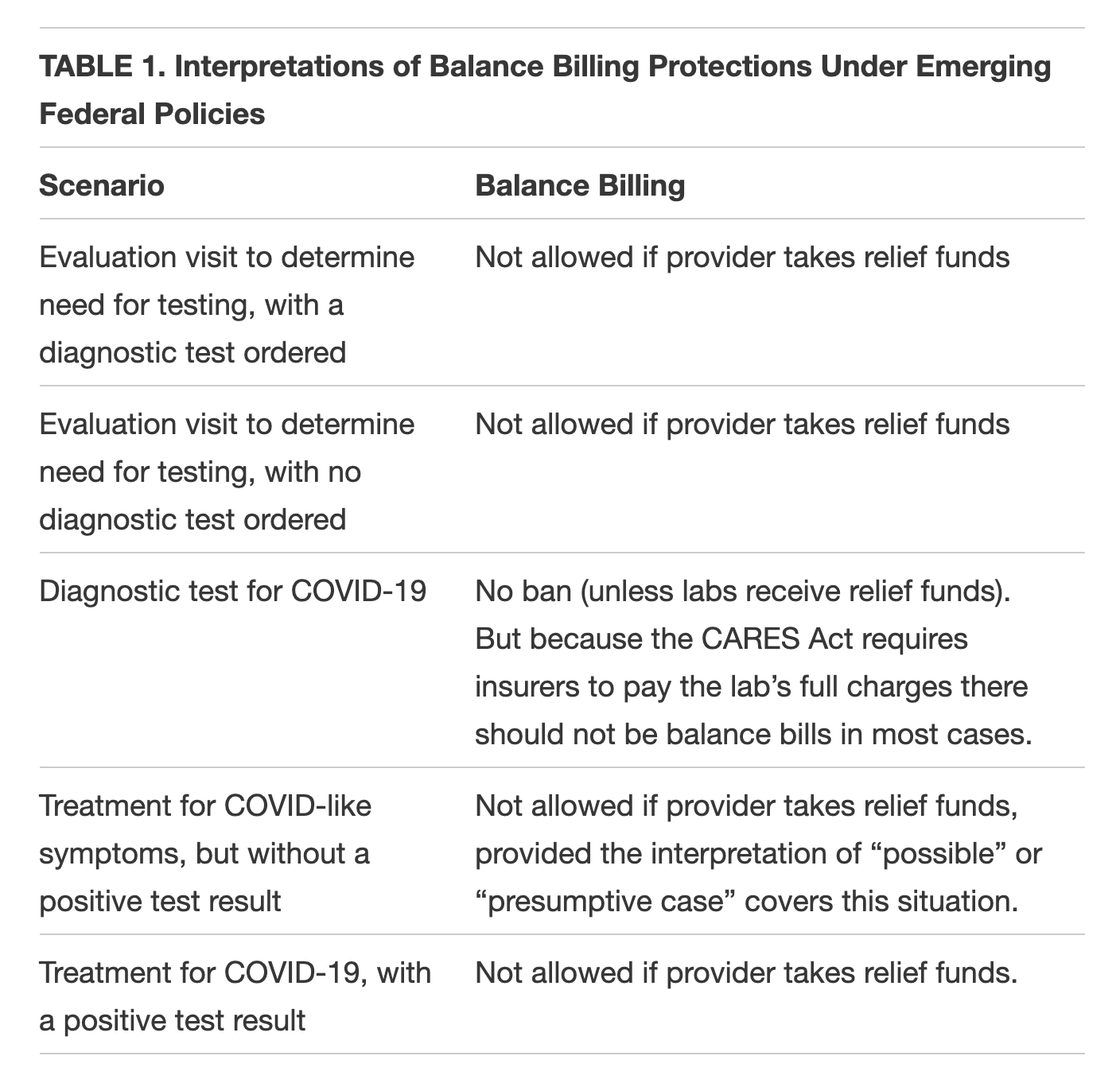

Under the PRF, the U.S. Department of Health and Human Services (HHS) terms and conditions state that the balance-billing protection applies to “all care for a possible or actual case of COVID-19.” Notably the announcement of a second round of funding instead uses the phrase “presumptive or actual COVID-19 patient.” The use of the term “presumptive” instead of “possible” suggests that HHS intended to narrow the types of patients eligible for protection. As shown in Table 1, patients with COVID-19 symptoms, but without a positive test result, could fall outside the PRF protections.

Regarding evaluation and diagnosis, HHS has issued limited guidance to providers receiving PRF funds. A commonsense interpretation would suggest that HHS intends to include as possible cases those patients who see a health professional (whether in person or through a virtual visit) or go to an emergency room thinking they may have COVID-19, regardless of whether a test is eventually ordered. Furthermore, common sense says that the protection would include testing for influenza or other alternative diagnoses as part of the evaluation visit.

Regarding treatment, it seems clear that protections continue for any patient for whom the test result is positive or presumptive positive for COVID-19 or the provider documents that the patient has COVID-19. But the rules are unclear if there has not been a positive test result. One interpretation of either the “possible or actual case” or “presumptive or actual” language is that such a patient would qualify. But this interpretation is not explicit in HHS documents.

There are questions for other common situations for patients. For example, do the rules protect patients who have symptoms but who later test negative for COVID-19? It depends on the definition of “presumptive case.” If the test is negative, is balance billing prohibited for services delivered up to the point of the negative test result?

A final question about the scope of these protections: How long will these rules be in effect? If they are linked to the national emergency declaration, does the protection end when the emergency declaration is ended? Or will the ban on balance billing apply permanently for providers who receive the PRF funds?

Are All Providers Banned from Balance Billing?

Providers accepting money from the PRF are banned from balance billing. But to understand the breadth of protections, we need to know the range of providers covered.

The initial round of federal funds (30 percent of the original funds) was distributed on April 10 to facilities and providers who received Medicare fee-for-service reimbursement in 2019 and who “provided diagnoses, testing, or care for individuals with possible or actual cases of COVID-19.” HHS notes that “care does not have to be specific to treatment of COVID-19” and that “HHS broadly views every patient as a possible case of COVID-19.”

This first round of funding was clearly meant to go to a broad range of facilities and providers. But there are obvious gaps. Funding did not go to providers, such as many pediatric specialists or obstetricians, who do not receive Medicare payments. Nor did it go to providers whose Medicare patients are exclusively enrolled in Medicare Advantage plans. Also excluded in this round were providers whose patients are exclusively uninsured or covered by Medicaid.

The second round of federal funds, announced on April 22, fills some of the gaps in the scope of providers included in the first round of the PRF. The new round targets providers with a small share of Medicare fee-for-service revenue, providers in COVID-19 high impact areas, rural providers, providers treating uninsured patients, and other specified categories.

Even if relatively few providers are missed in the distribution of funds, at least after the second round, some could refuse the terms and conditions and thus not receive funds. Participation is hard to predict and could vary according to their payer mix, loss of elective patients, or number of COVID-19 patients.

It is also unclear how patients will be able to know if a provider treating them has agreed not to send balance bills. Indications from HHS are that there will not be a public database of PRF recipients, where patients can look up their provider. So will they have to ask about their hospital or doctor’s PRF status before receiving treatment?

Additionally, it is not clear that health professionals practicing in PRF-participating hospitals will be bound by the same terms and conditions if they do not also accept PRF funds; such physicians, if out-of-network, could still be permitted to balance bill patients. HHS has not yet issued guidance to address this question.

Another question is whether clinical labs and other provider types could also be recipients of PRF funds. The HHS announcement on April 22 notes that forthcoming, separate funding would include skilled nursing facilities, dentists, and providers that solely take Medicaid. If labs receive money from the PRF, they would be prohibited from balance billing patients for processing a COVID-19 test or requesting full payment upfront.

Can Consumers Be Required to Pay Upfront?

One key question is whether providers can demand that patients pay up front for services, with the onus on the patient to seek reimbursement from their insurer. There is already evidence that some providers conducting COVID-19 tests are collecting fees up front. Many patients will find it difficult to provide such advance payments, leading some to forgo testing or treatment.

HHS’ terms and conditions state the provider cannot seek to collect from patients “out-of-pocket expenses in an amount greater than what the patient would have otherwise been required to pay” in-network. Although this seems to say that the patient should not be billed in full upfront, there is not explicit ban on this practice.

What Will Out-of-Network Providers Be Paid?

Another question is what payment out-of-network providers will receive from insurers. Most proposals to ban balance billing include a means of determining payment. But the conditions attached to the federal PRF include no policy dictating what the insurer should pay to the out-of-network provider who is banned from balance billing.

The Affordable Care Act has a payment standard for emergency services, based on the greatest of 1) the median in-network negotiated rate; 2) Medicare rates for emergency services; or 3) a method used to determine the cost of non-network care (such as usual, customary, and reasonable (UCR) charges) with in-network cost-sharing rules. This latter method would apply for any services considered to be emergency services. For any services to treat a stabilized patient, the ACA sets no payment standard.

Some states with laws protecting patients from balance bills include a payment standard or independent dispute resolution process. And a few states have added protections specific to the pandemic. For health insurance subject to state regulation, these laws should dictate payment for COVID-related cases.

Lastly, emergency rooms, clinics, and hospital-employed physicians often charge facility fees in addition to charges for professional services. Although the HHS’ guidance to date does not address whether facility fees are subject to balance billing restrictions, the language seems to imply that protections apply here as well.

How Can the Balance Billing Ban Be Enforced?

The terms and conditions for the PRF funds do not articulate how the ban on balance billing will be enforced. This is also an issue for states that have laws prohibiting balance billing in emergency or other situations. Many states have struggled to find effective mechanisms to enforce their protections. Although there is some basic compliance and disclosure language in the terms and conditions, there is no clear mechanism for HHS to assess how providers are – or are not – complying with the ban on balance billing. Nor has there been any discussion to date of how violations will be adjudicated or punished. If patients receive balance bills and are not aware that they have no obligation to pay, they may pay the bill or fear being sent to collections.

Looking Forward

Patients should not fear that they will receive surprise medical bills if they seek diagnosis, testing, or treatment for COVID-19; such fears could lead to delays in seeking health services, which in turn could pose a considerable public health risk. A few states have acted to require private insurance companies to cover and waive cost-sharing for COVID-19 treatment, but not all of these impose a companion requirement on providers to refrain from balance billing patients. The federal government, through the PRF, has placed a critical restraint on providers’ ability to balance bill, but HHS needs to provide greater clarification of the scope and scale of these protections.

This blog was originally posted from the Georgetown Center on Health Insurance Reforms.