As families lose their jobs and employer-sponsored health insurance, eliminating Children’s Health Insurance Program (CHIP) premiums is a great way to provide continuity of coverage for children and fiscal relief for families. But there may be a catch. While some states are submitting state plan amendments to waive collection of premiums or temporarily halt disenrollments for nonpayment of premiums, it is difficult to get a clear picture of exactly what states are doing.

According to our tracking through a variety of sources, more than a dozen states have plans to waive or suspend premium payments in some way. But the devil may be in the details. What does it mean to suspend premiums? Are states waiving premiums completely or just not collecting them during the public health emergency? Will families be required to catch up on late payments at some later date? What does “at state discretion” mean? Will premiums be waived on a case-by-case basis or across the board? How do families know if they are not required to pay premiums?

First the basics: There is no requirement for CHIP programs to charge either premiums or cost-sharing when enrollees use health care services. Of the 35 states with separate CHIP programs, 22 states charge monthly or quarterly premiums and four states charge annual enrollment fees. Additionally, four states without separate CHIP programs also charge premiums to CHIP-funded kids in Medicaid. (See Tables 13 – 15 in the 50-state Medicaid survey.) Premiums often vary by income or family size.

Some states charge a family premium, regardless of the number of children in a family, while other states set a family maximum cap (i.e., the individual child rate X three children). Individual child monthly premiums range from a low of $11 per month per child to a high of $98, while family-based premiums range from $10 to $235 (for a family of four; higher for larger families). The latter represents Missouri’s premiums which are based on the federal poverty level and updated every year using a complicated formula that resembles how federal taxes are calculated. In some states like Pennsylvania and Wisconsin, where the highest premiums are $84 and $98 respectively, there is no family maximum. If you’re paying $98 for four kids, your monthly cost is $392. In all states, the total out-of-pocket cost-sharing for the family cannot exceed 5 percent of family income.

A few states – specifically Pennsylvania and New York – appear to be waiving premium collection or not disenrolling children for nonpayment but that doesn’t mean families are off the hook. In fact, New York only asked (but didn’t require) the CHIP health plans that directly collect premiums to ‘refrain’ from disenrolling CHIP kids for nonpayment. Pennsylvania took a slightly stronger stance and will not allow CHIP plans to disenroll children for nonpayment but families will still be financially responsible for paying their premiums at some point.

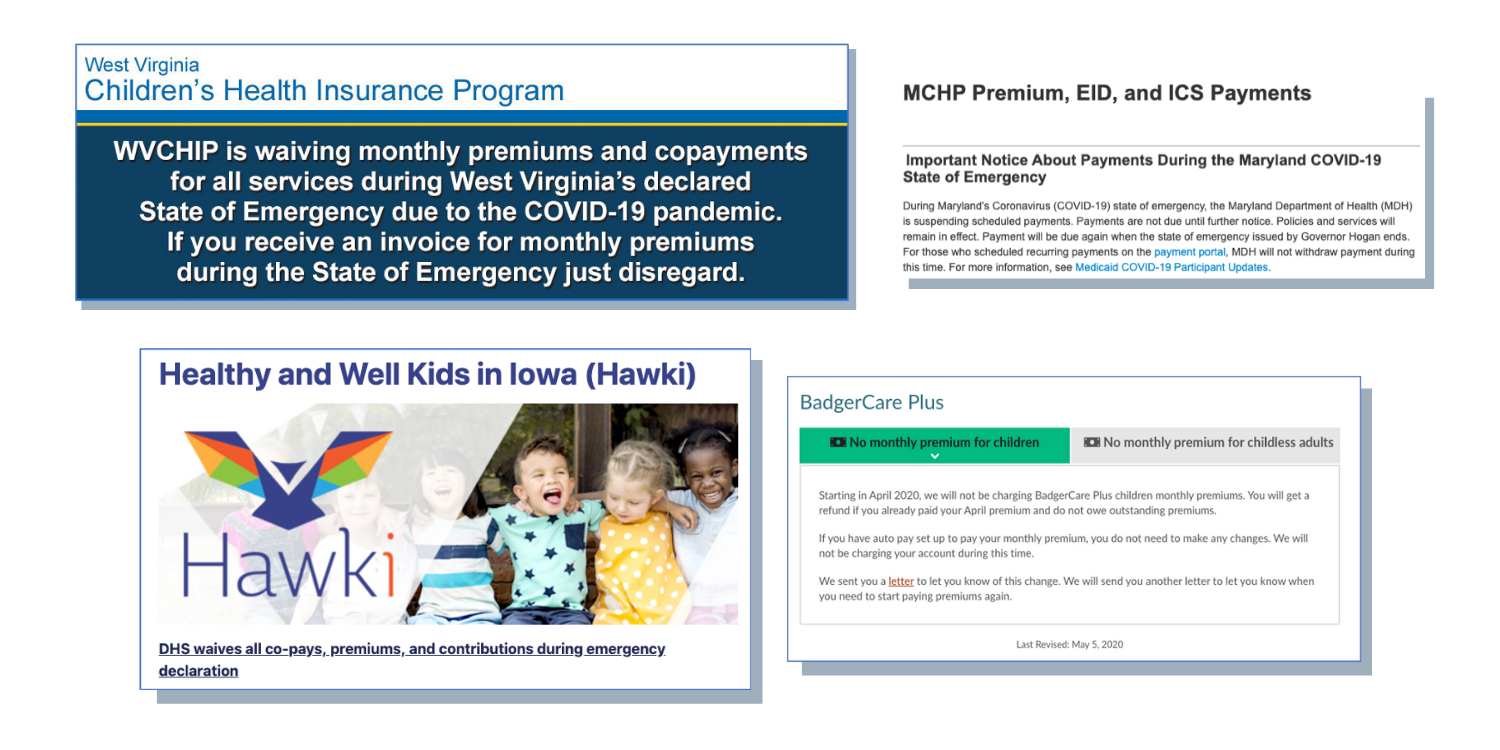

On the other end of the spectrum, Iowa, Maryland, West Virginia, and Wisconsin have taken proactive steps to cease all premiums during the state of emergency. These states have prominent notices on their websites noting that premiums are waived during the public health emergency.

At “state discretion” or “may waive premiums” are not definitive statements and do no clearly communicate premium payment policies. There are few reports from the field of states that plan to waive premiums (DE, IL, IN, NJ, UT, and VT) but we have yet to see CMS’ approvals on these actions. Then there are a number of states (AZ, CA, GA, KS, LA, ME, and NC) that have existing or new “evergreen” state plan provisions or have received temporary approval through CHIP disaster state plan amendments (SPA) that indicate “at state discretion,” the state “may” waive premiums. That doesn’t sound definitive to me. Moreover, I’m not seeing any notice to applicants or enrollees on most state websites. However, it is somewhat reassuring that these SPAs usually waive disenrollment policies and lockouts for nonpayment in the 14 states that prevent kids from re-enrolling for a period of time when their families are unable to meet premium obligations.

States could receive at least 80 cents in federal funding for every premium dollar waived. This is an important point. If states were to eliminate premiums, they would receive federal match for the amount of money that families would have paid. Currently, for the rest of 2020, this means that states would receive at least 80 cents from the federal government for every dollar that families would contribute toward the cost of their children’s coverage. The reason is that premiums paid by families offset the cost of state expenditures before the state can request reimbursement for the federal share. If states don’t charge premiums, they get federal match on total expenditures. (See SSA Section 2015(a)(5).) Frankly, states could easily spend more on administrative expenses trying to collect premiums than they recoup from families struggling to make ends meet during the public health and economic crises we are now facing.

Too many questions, and too few answers. The fact is, unpaid premiums may add up over time and families could end up owing hundreds of dollars when the temporary changes to payment policies expire after the public health emergency is lifted, even if their economic situations haven’t improved. And it is simply not clear whether states are actually not charging any enrollee premiums or simply not disenrolling children for nonpayment during the public health emergency. Will families be required to repay outstanding premiums when the emergency is lifted or are premiums being forgiven? States owe it to families to be clear and transparent about their payment policies. And the best policy is to support continuity of coverage for children and give families a helping hand by waiving premiums for all children.